Yes, Day trading is legal in Canada. However, the Canada Revenue Agency (CRA) typically classifies frequent trading as business income (taxed at 100%) rather than capital gains (50-66.7% inclusion). Day trading within a TFSA is highly restricted; if the CRA deems the activity a “business,” all gains become fully taxable, and tax-free status is revoked.

How Does the CRA Tax Day Trading Profits in Canada?

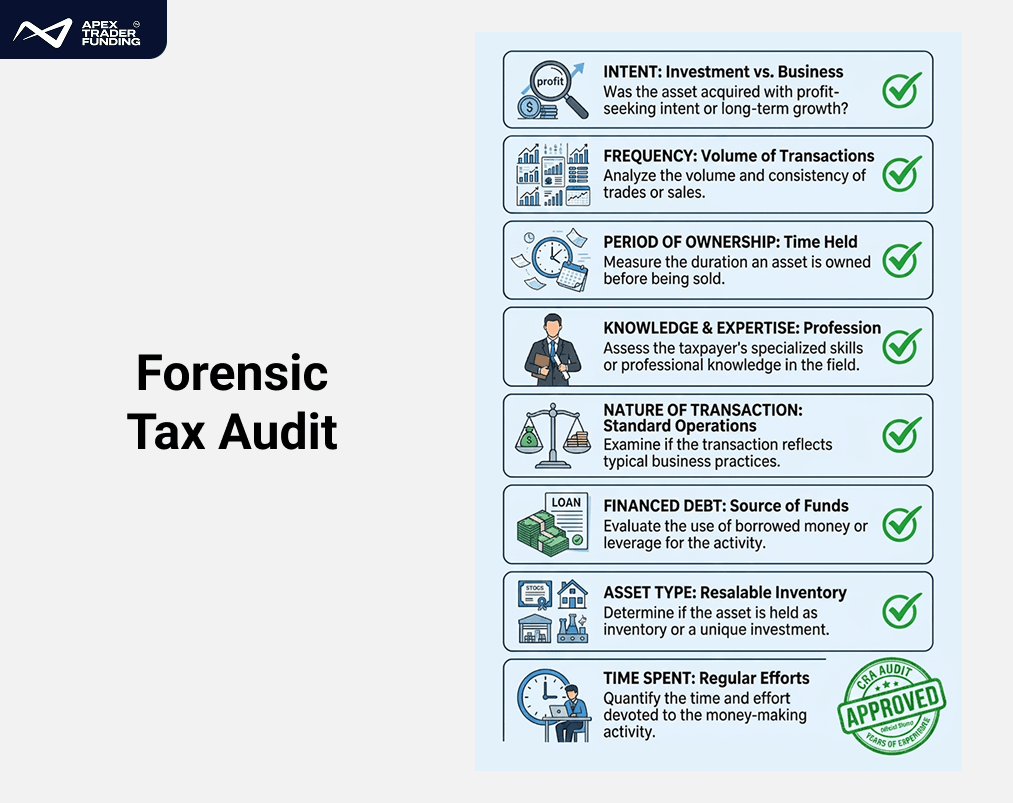

Yes. In 2026, the Canada Revenue Agency (CRA) classifies frequent, high-volume intraday trading as business income taxed at a 100% inclusion rate, rather than capital gains. This classification applies to any account—including TFSAs—if the activity reflects professional intent, high trade frequency, and short holding periods. Day trading taxation is determined by the “Adventure in the Nature of Trade” test, which reclassifies investment activity as a business based on trade frequency, intent, and professional knowledge. In 2026, if your activity is deemed a business, you lose access to the 50% (or 66.7% for gains over $250,000) capital gains inclusion rate.

The official framing allows Canadians to open a brokerage account and trade freely with no legal restriction on intraday activity. In practice, the tax treatment diverges sharply from what most beginners assume. When I reviewed the CRA’s position on frequent trading, the determining factor was not the account type but the pattern of behavior. The CRA evaluates patterns of behavior, not a single threshold. High trade frequency, short holding periods, and professional tooling are among the factors that collectively inform a reclassification review; there is no bright-line trade count.

In practice, accounts showing a consistent pattern of high-frequency turnover and significant growth face a targeted review. The CRA establishes its authority for these audits through the Income Tax Act (Section 9) and CRA Folio S3-F9-C1, which details the specific factors used to distinguish business income from capital gains. Reading the folio directly is worthwhile — it is written in plain language and makes the CRA’s reasoning transparent.

Experienced traders know that the CRA specifically audits for professional markers: the use of advanced platforms (like DAS Trader), CIRO-regulated margin levels — set by the Canadian Investment Regulatory Organization to govern how much investors can borrow to trade — and high-frequency “scalping” patterns (rapid-fire trading to capture small, repeated gains).

| Trading Scenario | CRA Classification | What Actually Happens |

| Infrequent trading with long holding periods | Capital gains — 50% inclusion rate | Lower tax exposure; activity treated as investment rather than commerce |

| Frequent intraday trading in a non-registered account is documented as a business | Business income — 100% inclusion, but expenses are deductible | Platform fees, data costs, and margin interest can be offset against gross gains |

| Frequent intraday trading inside a TFSA | Business income — 100% inclusion, no expense deduction | Tax-free status may no longer apply, including for prior years; 100% of gains are taxed as business income; losses are NOT deductible. |

One underappreciated advantage of business classification: if the CRA determines your trading activity constitutes a business, you lose the capital gains inclusion rate — but you gain the ability to deduct legitimate business expenses against your gross trading income. Platform subscription fees, real-time data feeds, margin interest (currently 8–11% at most Canadian brokers), home office costs, and relevant courses or software can all reduce your taxable income. A trader generating $80,000 in gross trading income with $15,000 in documented expenses is taxed on $65,000, not $80,000. This does not make business classification desirable, but it does mean professional structure and thorough documentation materially reduce the tax impact.

The TFSA Risk That Most Canadian Beginners Never See Coming

Among the more significant compliance risks for new Canadian traders is the TFSA reclassification — a scenario where profitable trading activity generates a meaningful tax liability that the account holder did not anticipate.

The potential impact is significant: a trader who makes $50,000 inside a TFSA through frequent intraday trading and receives a CRA audit faces taxation at approximately 53% in Ontario on the full amount. That is a $26,500 tax bill on money that was assumed to be completely protected. The TFSA space used to generate those profits is also permanently gone, meaning the trader loses both the gains and the ability to shelter future income in that account.

A second consideration worth understanding is the Superficial Loss Rule (Wash Sale). The Superficial Loss Rule states that if you sell a security at a loss and buy it (or an “identical” asset) back within 30 days, that loss is denied for tax purposes. For day traders who constantly cycle in and out of the same stock symbols, or tickers, this can lead to taxable income that exceeds net cash retained, because disallowed losses are excluded from the calculation, while gains remain fully included.

The T5008 Slip: Canadian brokers usually issue a T5008 slip that often defaults to capital gains reporting. The more reliable approach is to calculate your Adjusted Cost Base (ACB)—the total cost of your investment, including commissions—yourself, using your own trade records. A good trade log covers the date and time of each trade, your entry and exit price, position size, and a brief note on why you took the trade. With that information, your ACB calculation reflects the actual tax rules — not just the broker’s default output. Relying solely on T5008’s default figures often triggers an automated CRA mismatch audit because it fails to account for disallowed superficial losses.

The Strategic Value of a Forensic Trade Log

A forensic trade log is the single most important habit a serious Canadian trader can build. It is not a backup document for audits — it is the primary record that separates disciplined trading from speculation. Over time, this record becomes a performance database: you can see which setups work, where you overtrade, and whether your actual behavior matches your stated strategy. Traders who maintain this kind of log consistently make better decisions, because the log makes it harder to repeat mistakes and easier to prove what you intended from the start.

Expert Insight: The 2026 Regulatory Delta

Since IIROC merged into CIRO (Canadian Investment Regulatory Organization), the rules around margin and intraday trading have been updated and are more consistently enforced. Under the current framework, brokers are required to monitor intraday margin positions in real time.

If you are trading in a non-registered account and keeping a proper trade log, this works in your favour. Documented business intent means your margin interest — which runs between 8% and 11% at most Canadian brokers — is a legitimate tax deduction. The traders who benefit most from these rules are simply the ones who keep clean records from the start.

Enforcing strict risk management protocols and protecting core equity are the true hallmarks of an experienced trader. Focusing on capital preservation helps individuals protect their portfolios from the rising costs of high interest rates. Ultimately, understanding how to minimize trading costs and platform limitations and maximize the utility of every dollar is what separates sustainable, long-term market operations from short-term retail speculation.

Final Thoughts

Canadian tax law does not penalize active traders — it asks them to be honest about what they are doing. Traders who operate with clear intent, documented records, and consistent risk management are well-positioned under these rules. The CRA’s framework distinguishes between investors and business operators because the two activities genuinely are different. Understanding which category applies to you, and building your structure accordingly from day one, is not a burden — it is what professional trading looks like in practice.

To mitigate audit risk, many traders choose to register their activity as a business in a non-registered account and treat the TFSA as a “Long-Term Only” zone. Documenting every cost and decision from day one means that if the CRA ever reviews your “Adventure in the Nature of Trade,” you have the forensic records to defend your deductions with confidence.

For traders who want to separate their active intraday strategy from their personal registered accounts entirely, evaluation-based funding platforms offer a structurally clean alternative. Trading with external capital means your high-frequency activity never touches your personal brokerage profile or TFSA room.

Check out the official Apex Trader Funding site and choose account options like the 25K WealthCharts EOD Trail or 25K Rithmic Intraday Trail to access institutional-grade tools that help you build a statistically robust edge.