Trading discipline is a risk management system designed to protect a trading account from major losses. It utilizes concepts such as the Risk of Ruin, position sizing rules, and daily loss limits to reduce emotional decision-making, preserve capital units across losing streaks, and build the structural foundation needed to compound gains consistently.

Discipline in Trading Is Misunderstood at the Most Expensive Level

When viewed through the lens of risk management mathematics, trading discipline takes on a broader meaning than emotional control alone. Discipline is often discussed as a psychological skill developed through patience, consistency, and self-awareness. While those qualities are important, there is also a measurable risk-management component.

From a mathematical perspective, discipline helps traders maintain the conditions required for their strategy to perform as intended over time. Consistently following position-sizing rules, risk limits, and trade-management guidelines can help reduce the likelihood of drawdowns becoming disproportionately large relative to account size. In this sense, discipline is not only a behavioral trait—it is also a practical framework for preserving consistency and managing long-term risk.

Analysis of the Risk of Ruin formula using real trading scenarios highlights an important principle: even strong trade selection cannot consistently overcome the effects of excessive position risk. This is why disciplined position sizing is considered a foundational element of risk management. By keeping risk exposure aligned with account size and strategy objectives, traders can better preserve capital and maintain consistency over time.

Before deploying capital, a trader should establish a predefined stop-loss level. A stop-loss is an order designed to help limit losses by triggering an exit when the price reaches a specified threshold. While stop-loss orders can automate risk management, they do not guarantee execution at the exact stop price. During periods of extreme volatility, market gaps, or reduced liquidity, execution may occur at a less favorable price due to slippage.

When a market gaps beyond a stop-loss level, the resulting execution may occur at the next available market price rather than the intended stop price. This illustrates why risk-management rules should be established before periods of heightened volatility occur.

At the same time, even the most objective risk-management framework depends on consistent execution. Position-sizing rules, stop-losses, and risk limits are only effective when they are followed. In practice, mathematics and psychology work together: sound risk parameters provide the structure, while discipline helps ensure that structure is maintained during changing market conditions.

Risk of ruin, position sizing, and equity curve behavior are often viewed as advanced topics, but they form an important part of a trader’s risk-management foundation. Understanding these concepts can help traders make more informed decisions about risk, capital preservation, and long-term consistency. In that sense, they help transform trading from a process driven primarily by intuition into one guided by structure and defined risk parameters.

How Does the Risk of Ruin Equation Calculate Account Survival?

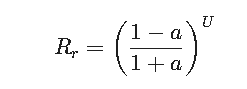

The Risk of Ruin equation calculates the statistical probability of account survival by factoring in a trader’s win rate, loss rate, risk-to-reward ratio, and the size of individual risk units. When trade sizes scale without a defined limit, available capital units decline sharply. As these units shrink, the probability of ruin rises exponentially with each subsequent trade.

The formal Risk of Ruin (Rr) formula is used to mathematically define account survival probability:

Where:

- a = p – q (Your statistical edge, where p is the win rate and q is the loss rate or 1 – p)

- U = Total trading capital units relative to risk per trade

Understanding this requires mastering the concept of Notional Exposure, which represents the total contract value controlled rather than the margin deposit. For example, if an account balance is $10,000 and a trader loses $1,000 by holding a position through a 20-point drop in the E-mini S&P 500 futures market (where one point equals $50), the new balance becomes $9,000. This pushes the account into a 10% drawdown from a single undisciplined trade. Drawdown is the percentage drop from an account’s peak balance to its lowest point before recovery.

In many Risk of Ruin models, the variable U represents the number of risk units available within a trading account and is influenced directly by position sizing. Because of this relationship, risk-per-trade decisions have a measurable effect on account durability over time.

For example, a trader risking 1% per trade on a $50,000 account maintains substantially more risk units than a trader risking 10% per trade on the same account. As the number of available risk units declines, the account becomes more vulnerable to the effects of normal losing streaks and larger drawdowns. This is one reason disciplined position sizing plays such an important role in managing risk and supporting long-term trading consistency. To maintain the high U variable required by the Risk of Ruin equation, the exact market allocation is determined using the standard Position Sizing Formula:

For example, if an account balance is $50,000 and the goal is to risk a disciplined 1% ($500) on an E-mini S&P 500 (ES) trade with a 4-point stop-loss ($200 per contract), the formula dictates: $500/$200 = 2.5 contracts. Rounding down to 2 contracts protects the absolute risk ceiling.

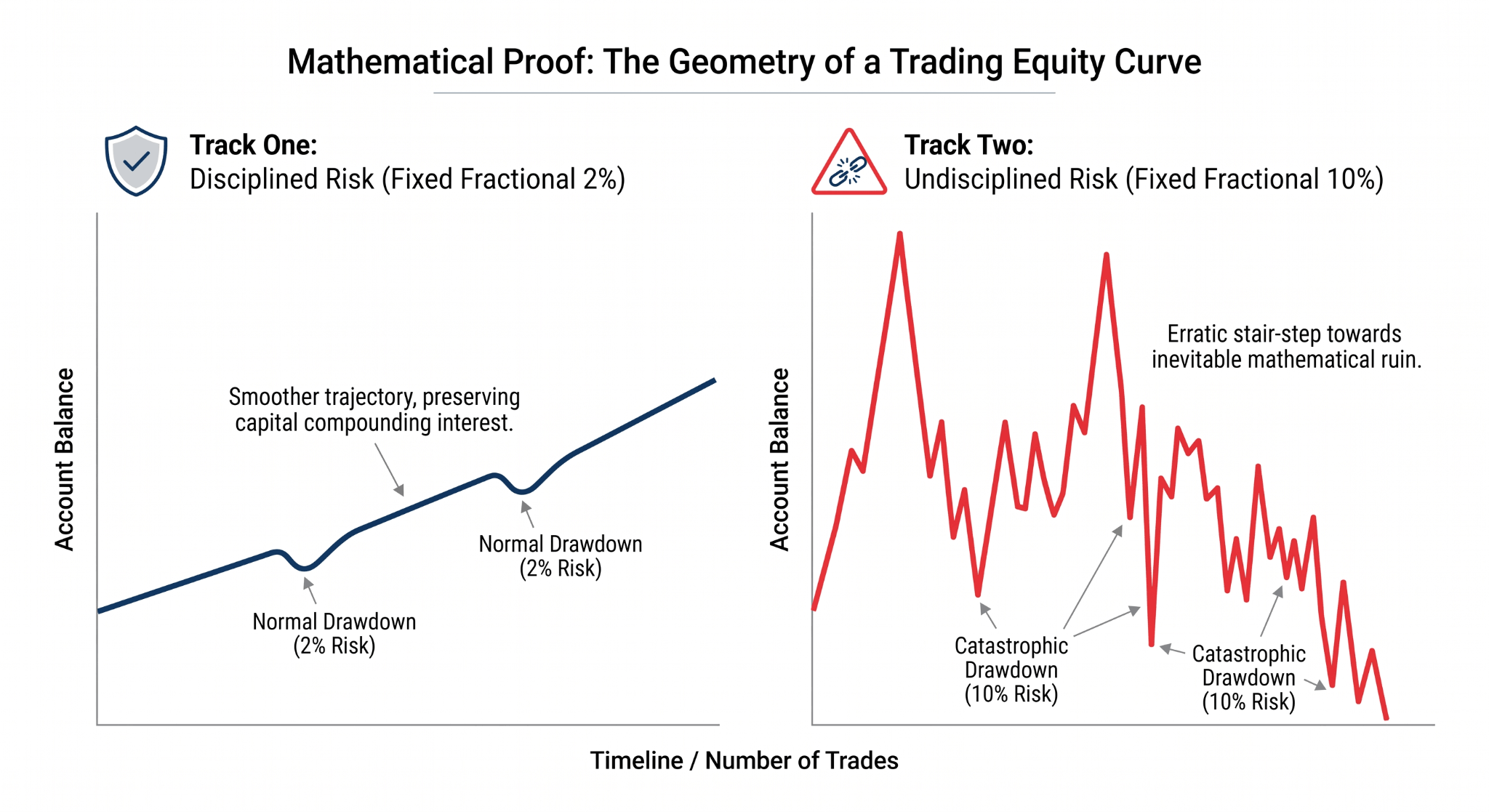

Applying consistent position-sizing rules can have a meaningful impact on the behavior of a trading equity curve—the graphical representation of an account’s value over time. By keeping risk exposure aligned with account size and trading objectives, traders may be better positioned to manage drawdowns and maintain more consistent performance characteristics.

Conversely, inconsistent position sizing can increase the magnitude of drawdowns and lead to greater variability in account performance. Over time, larger drawdowns require proportionally larger gains to recover, which is one reason position sizing is widely regarded as a core component of risk management.

A well-managed equity curve tells a story of consistent risk management rather than the absence of losses. When position sizing remains disciplined and aligned with a trader’s risk tolerance, drawdowns are often more manageable relative to account size, helping preserve capital for future opportunities.

This is one of the key objectives of disciplined position sizing: not avoiding losing trades altogether, but ensuring that normal losing periods do not have an outsized impact on a trader’s ability to continue executing their strategy over time.

What Discipline Looks Like When It Is Applied to a Live Account?

Monitoring trading discipline in practice often involves paying close attention to both trade-level and account-level risk metrics. Before entering a position, traders may evaluate the amount of capital at risk relative to account size. Throughout the session, they may also monitor realized losses and overall account performance to ensure trading activity remains within predefined risk parameters.

Many traders choose to establish daily loss limits and other risk controls before placing trades. By defining these boundaries in advance, they can create a more structured framework for managing risk throughout the trading session.

The E-mini S&P 500 futures contract (ES) provides a useful example of how risk management can affect account outcomes. Because each point in ES represents $50 per contract, position size and stop placement can have a meaningful impact on account performance.

For example, a trader with a $10,000 account who places a stop-loss 4 points from entry would limit risk to approximately $200 per contract. If the stop is reached, the loss is predefined, and capital remains available for future opportunities. By contrast, allowing a position to remain open beyond the original risk parameters can expose the account to substantially larger losses during periods of increased market volatility.

This illustrates why many traders incorporate predefined risk limits, stop-loss orders, and account-level safeguards into their trading process. These controls are intended to help manage downside exposure and preserve capital during adverse market conditions.

| Feature | Hard Data | What it Protects |

| Disciplined risk per trade | 1–2% of total account equity | Keeps capital units high enough that a losing streak cannot trigger exponential ruin probability |

| Undisciplined risk per trade | 10% of total account equity | Reduces capital units to 10 on a $50,000 account — ruin probability rises in proportion to each unit of capital lost. |

| Hard daily stop threshold | 5% of total capital | Breaching this triggers a session lockout — prevents revenge trading from compounding a single bad session into a multi-day recovery problem |

| Overnight financing cost | Compounding swap rates apply per session held | A losing position held overnight accumulates financing drag on top of the unrealized loss, raising the recovery threshold daily. |

How Traders Lose Discipline Without Realizing It?

Many of the discipline challenges that affect traders do not begin with a dramatic mistake. More often, they begin with small departures from a trading plan that seem insignificant in the moment but accumulate over time.

A common example is remaining in a position after the original reason for entering the trade no longer exists. Instead of reassessing the setup objectively, a trader may delay making a decision and allow the position to remain open in the hope that market conditions will improve. While patience can be a valuable trading skill, failing to reevaluate risk as conditions change can expose an account to larger losses than originally intended.

Discipline is not only about making good decisions. It is also about making timely decisions when market conditions no longer support the original plan.

Two Approaches to a Losing Streak

One of the clearest differences between disciplined and undisciplined trading can be seen in how traders respond to a series of losses.

Scenario A: The Reactive Approach

A trader experiences several consecutive losses and decides to increase position size in an attempt to recover more quickly. While the intention may be understandable, increasing risk after a losing streak can amplify drawdowns at a time when additional caution may be warranted. If market conditions have shifted away from the trader’s strategy, larger position sizes can magnify losses before the underlying issue has been identified.

Scenario B: The Systematic Approach

A trader experiences the same series of losses but responds by reviewing recent trades, reassessing market conditions, and reducing risk exposure until performance stabilizes. By preserving capital during periods of uncertainty, the trader maintains flexibility and remains positioned to participate when conditions become more favorable.

The key difference is not confidence or conviction. It is the presence of a predefined process that guides decision-making when emotions are most likely to influence behavior.

Why Rules Can Be an Advantage

Some traders view risk-management rules as limitations. In practice, many experienced traders view them as tools that help create consistency.

Predefined risk limits, position-sizing guidelines, and trading pauses can reduce the likelihood of emotionally driven decisions during periods of stress. Rather than forcing traders to make difficult decisions in the heat of the moment, these rules establish boundaries before trading begins.

The purpose of a risk-management framework is not to eliminate losses. Losses are a normal part of trading. Instead, the objective is to help ensure that individual trades or short-term setbacks do not have an outsized impact on long-term performance.

The Role of Daily Risk Limits

Many traders choose to establish a maximum amount they are willing to lose during a single trading session. Once that threshold is reached, trading activity may be paused for the remainder of the day.

The benefit of a daily risk limit is not that it prevents losses entirely. Rather, it can help prevent a difficult trading session from developing into a significantly larger drawdown driven by frustration, urgency, or the desire to recover losses quickly.

By defining these limits in advance, traders create a structured decision-making framework that remains in place regardless of market conditions.

The Connection Between Position Size and Discipline

Position sizing is one of the most important risk-management decisions a trader makes because it influences the impact of every trade on the overall account.

When position sizes are larger than a trader’s risk tolerance or account size can reasonably support, even normal market fluctuations can create emotional pressure. That pressure may increase the temptation to move stop-loss levels, hold positions longer than planned, or deviate from established trading rules.

Conversely, when position sizes remain aligned with predefined risk parameters, traders may find it easier to follow their trading plan consistently. Smaller and more manageable risk exposure can help support objective decision-making during both winning and losing periods.

Discipline as a System

Discipline is often described as a matter of willpower. While mindset plays an important role, many successful traders view discipline as a system rather than a personal trait.

Position-sizing rules, predefined risk limits, stop-loss levels, and trade review processes create a structure that supports consistent decision-making. These tools cannot eliminate uncertainty or guarantee positive outcomes, but they can help traders manage risk more effectively and navigate changing market conditions with greater consistency.

Ultimately, discipline is not about avoiding losses. It is about creating a framework that allows a trader to continue executing their strategy through both favorable and unfavorable periods while preserving the capital needed to participate in future opportunities.

The Tactical Connection Between Position Size and Overnight Cost

Position sizing influences more than potential profit and loss. It also affects how traders respond when a position moves against them.

When risk exposure is larger than a trader is comfortable managing, normal market fluctuations can create pressure to deviate from a trading plan. Traders may be tempted to hold positions longer than intended, adjust predefined exits, or increase risk in an attempt to recover losses. In many cases, the position-size decision made at trade entry influences the quality of every decision that follows.

For this reason, many traders establish risk parameters before entering a position. By defining acceptable risk in advance and sizing positions accordingly, they create a framework that can support more consistent execution during both favorable and unfavorable market conditions.

Discipline is often associated with willpower, but risk management is equally important. Position-sizing guidelines, stop-loss levels, daily risk limits, and account-level controls help create a structure that supports objective decision-making when market conditions become challenging.

Why Risk Controls Matter

One of the primary goals of risk management is not to eliminate losses, but to ensure that losses remain proportionate to the trader’s overall account objectives and risk tolerance. Predefined controls can help reduce the likelihood that a single trade or a difficult trading session has an outsized impact on long-term performance.

Many professional trading environments utilize risk-management frameworks that include account-level safeguards, predefined drawdown thresholds, and trading restrictions designed to reinforce disciplined execution. These controls are intended to help traders focus on consistency, capital preservation, and long-term development rather than short-term recovery attempts.

Traders evaluating funded-account programs may benefit from understanding how different firms structure their risk-management rules, including daily loss limits, drawdown methodologies, and account-monitoring controls. These parameters are often designed to encourage disciplined trading practices while helping manage overall account risk.